Everyone with spare money faces the same choice. Do you keep it safe in a savings account, or do you invest? We’ll list the pros and cons and help you determine what suits you best.

Everyone with spare money faces the same choice. Do you keep it safe in a savings account, or do you invest? We’ll list the pros and cons and help you determine what suits you best.

Important to note: investing involves risks. You may lose part of your investment. Past performance does not guarantee future results. The information in our blogs is general and not personal investment advice.

Saving is the most well-known and trusted way to set money aside. Saving is easy, safe, and flexible.

With saving, you run almost no risk. Your money in a savings account is protected up to €100,000 per bank. This means: if a bank goes bankrupt, you’ll always get that amount back from the central bank. Do you have more than €100,000? Then you can distribute it across multiple banks. This way, you can’t really lose your savings.

You can withdraw your savings immediately. This comes in handy if you face an unexpected expense, or if you’re saving for a big purchase that’s coming up.

However, this comfort and safety come with a few drawbacks. The interest rate on savings is quite low, especially in recent years. As a result, your wealth hardly grows.

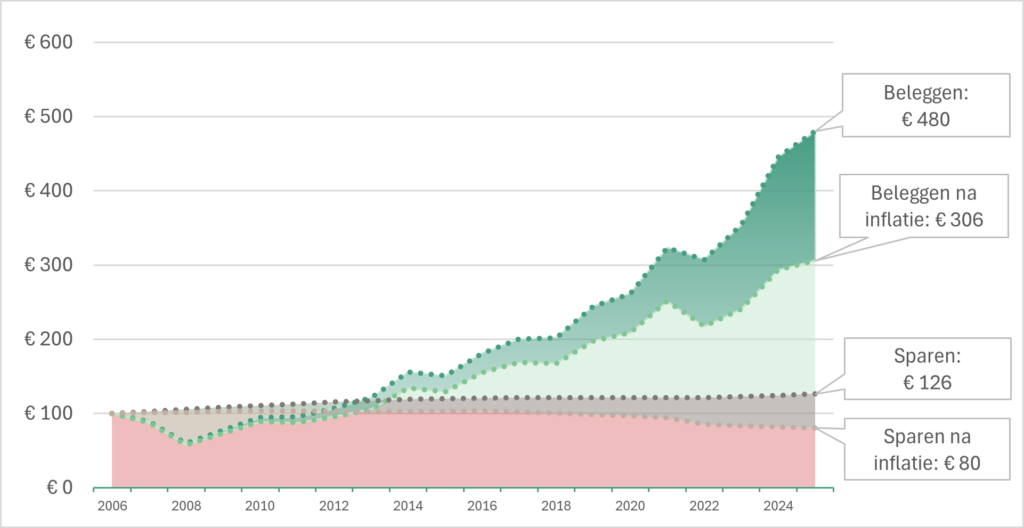

And even if your wealth grows slowly, you also need to consider inflation. Inflation means that prices rise and that you can buy less than before with the same amount. If the interest on your savings account is also lower than inflation, your account balance may increase, but you end up with less purchasing power.

This is an illustrative example of the return on investment in the global stock market and savings.

When investing, your deposit may become worth less. Past performance is no guarantee of future results. The equity portfolio consists of 8 ETFs (11% IE00BYX2JD69, 13% IE000Y77LGG9, 16% IE00BH4GPZ28, 10% LU0950674332, 15% IE00BHZPJ015, 8% IE00B52VJ196, 11% IE00BZ02LR44, 15% IE00BHZPJ239) from which the UpToMore costs of €0.99 p/m and 0.10% p/a have been deducted, resulting in a net return. This is a benchmark and not a historical fund return of UpToMore. UpToMore has been around since 2024. The return on savings comes from De Nederlandsche Bank and concerns freely withdrawable savings accounts. The inflation figures come from the Central Bureau of Statistics. Taxes are not included.

You can invest in various financial instruments such as stocks or bonds, or in investment funds. The goal is to achieve a return that’s better than the savings interest rate.

The advantages of investing mirror the disadvantages of saving. If you look at the past forty years, investing yields much more than saving. And the return was also higher than inflation.

This higher return makes an enormous difference compared to saving in the long term. This is explained by the effect of compound interest: you earn returns on what you earned last year. This way, the difference with saving keeps growing as time progresses.

From to in years of investing.

Investing involves risks. You may lose part of your investment if the stock market declines. With savings, you don’t face this risk. Past performance shown does not guarantee future results. They are based on long-term historical returns. Your actual results may vary. UpToMore does not provide investment advice.

Just as the advantages of investing mirror the disadvantages of saving, the same applies to the disadvantages of investing. Investing carries risks: the value of your investments can both rise and fall. So you need to be prepared that you might lose part of your investment.

To be able to absorb those dips on the stock market well, a long investment horizon is important – preferably ten years or longer. If you know that in advance and can set aside your money for at least that period, you will be better prepared. This way you can stick to your plan and calmly sit out the peaks and troughs.

For most people, it’s not about choosing between investing or saving but about the order: first saving, then investing.

Saving is the foundation for financial security. This allows you to cover unexpected costs, pay for large purchases, or for example, make a down payment on a house.

If you still have money left over that you can miss for a longer period of time – preferably ten years or longer – then you can start investing. Keep in mind that the value of investments can fall. But those who have consistently invested for the long term over the past decades rarely regret it.

Important to note: investing involves risks. You may lose part of your investment. Past performance does not guarantee future results. The information in our blogs is general and not personal investment advice.